While operating a mobile or home-based business comes with flexibility and cost savings compared to having commercial office, retail or factory space, it also introduces unique risks. As mobile businesses operate without a fixed business location, some mobile business owners may assume they are less likely to face liability claims, however accidents and incidents still occur. Similarly, some owners of home-based businesses they feel they have very little risk or liability risks may be covered in their standard home policy – this may not be the case. Commercial Public liability insurance may help protect mobile and home-based businesses from financial loss if a third party claims injury or property damage due to business activities.

While operating a mobile or home-based business comes with flexibility and cost savings compared to having commercial office, retail or factory space, it also introduces unique risks. As mobile businesses operate without a fixed business location, some mobile business owners may assume they are less likely to face liability claims, however accidents and incidents still occur. Similarly, some owners of home-based businesses they feel they have very little risk or liability risks may be covered in their standard home policy – this may not be the case. Commercial Public liability insurance may help protect mobile and home-based businesses from financial loss if a third party claims injury or property damage due to business activities.

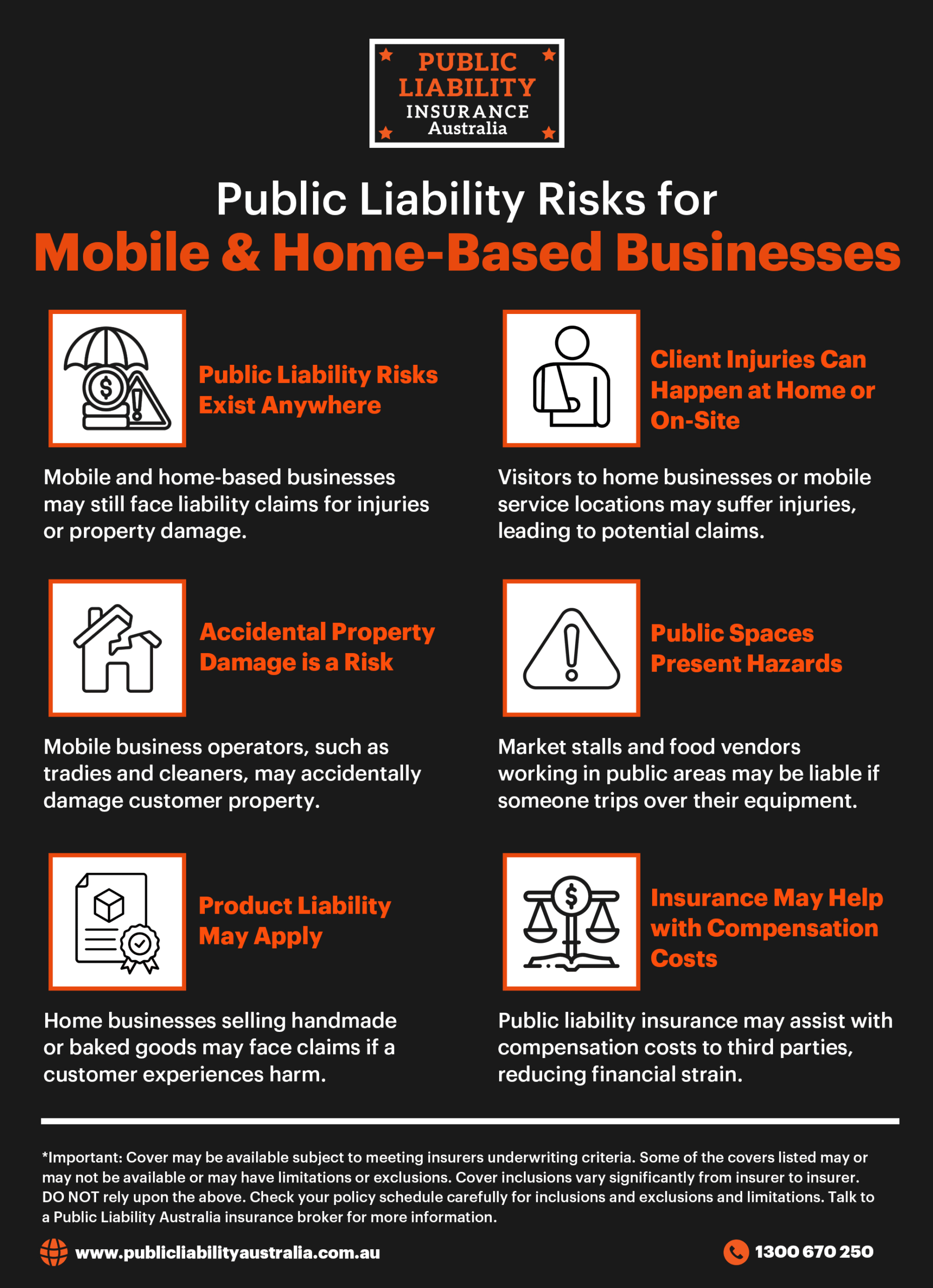

Risks Faced by Mobile and Home-Based Businesses

Customer Injuries at Your Home or On-Site

Home-based businesses, such as hairdressers, beauticians or consulting services, often welcome clients into their home. If a visitor trips over loose flooring, slips on a wet surface, or sustains an injury while on the premises, the business owner may be held liable for medical costs or compensation claims. This may not be covered in your standard home policy. Similarly, mobile businesses such as tradies, cleaners, and massage therapists work at client locations where accidents to third party persons and property can occur, potentially leading to costly claims.

Damage to Client Property

For mobile businesses working at customer locations, accidental property damage is a significant risk. A plumber may accidentally damage a client’s bathroom, a mobile mechanic could scratch a customer’s car, or a mobile pet groomer might damage a client’s furnishings These incidents may lead to expensive claims if the business owner is found responsible or must defend themselves in court.

Third-Party Incidents in Public Spaces

Some mobile businesses, such as market stall owners or food vendors, operate in public spaces. If a passerby trips over a piece of equipment the business may face liability claims. Public liability insurance may help cover compensation costs in such cases.

Product Liability Risks

Home-based businesses selling products, such as handmade goods or baked goods, may face product liability risks. If a customer suffers an allergic reaction, injury, or illness from using a product, they may seek compensation from the business. In Australia, as Product Liability insurance cover for most micro and small businesses is bundled with public liability insurance, to help with such claims.

Legal Costs from Unexpected Claims

Even when a mobile or home-based business owner follows best practices, claims can arise from unforeseen circumstances. Defending a claim can be costly, even if the business is not at fault. Subject to policy wording, public liability insurance may help cover legal costs associated with defending against third-party claims.

How Public Liability Insurance May Help

Public liability insurance may provide financial protection by covering legal expenses, compensation payments, and other associated costs if a claim is made against a mobile or home-based business. This may help ensure that a business can continue operating without the burden of unexpected financial strain.

While public liability insurance is not legally required in Australia for all businesses, some industries, contracts, or event organisers may require proof of coverage before allowing a business to operate in certain spaces.

Final Thoughts

Mobile and home-based businesses face unique risks that can lead to costly liability claims. Public liability insurance may offer peace of mind by providing financial protection against third-party injury or property damage claims. For guidance on suitable cover, business owners can speak with an insurance broker to explore their options.

Disclaimer: The content of this blog article is intended for general informational purposes only and should not be considered as professional advice. While we strive to ensure accuracy, we make no guarantees about the completeness or reliability of the information. For guidance regarding what and how much public liability insurance cover you need, we recommend consulting with a business insurance broker. Any actions you take based on any information provided here are at your own discretion.